Balancing education costs alongside everyday living requires realistic planning and regular review. Whether paying for primary schooling, vocational training, or continuing education, families and individuals benefit from a structured approach. The right strategy reduces stress and keeps learning goals achievable without derailing other financial priorities. This article outlines practical steps to assess, budget, and manage education expenses.

Assessing Current Costs

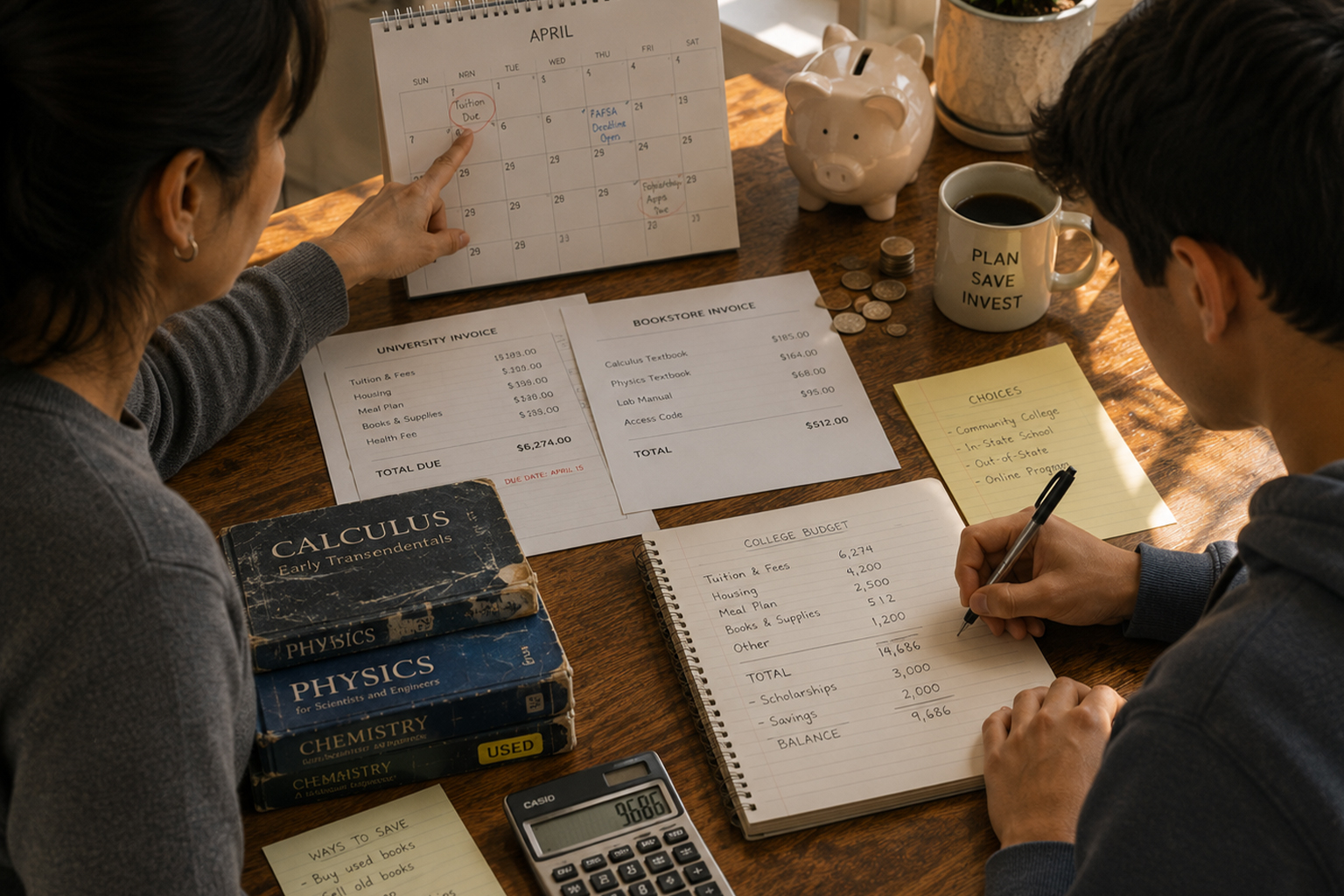

Begin by compiling a full picture of current and upcoming education costs. Include tuition, books, supplies, transportation, technology, and any associated fees, as well as indirect costs like childcare or lost wages. Tracking these elements for several months reveals patterns and peak spending periods that a simple calendar can miss. Accurate assessment makes it easier to set realistic savings targets and avoid unpleasant surprises.

- Tuition and fees

- Materials and books

- Housing and transport

- Childcare and lost income

Use this checklist to prioritize expenses and spot areas for early action. Small shifts in timing or sourcing can free up meaningful funds.

Creating a Flexible Education Budget

Translate the assessment into a purpose-driven budget that separates essential costs from discretionary ones. Allocate a monthly education fund and treat it like a recurring bill so savings build consistently. Factor in short-term reserves for irregular costs and a modest contingency to cover unexpected increases. Revisit allocations each enrollment period or semester to keep the plan current.

- Set a monthly savings target

- Create a short-term reserve

- Adjust allocations each term

A flexible budget reduces last-minute borrowing and helps compare financing options. It also provides clarity when choosing between program options.

Reducing and Managing Expenses

There are practical ways to reduce education spending without compromising outcomes. Seek scholarships, employer tuition assistance, or sliding-scale community programs; buy used textbooks or share resources; and evaluate online courses which can lower costs. Consider spreading study over a longer period to avoid large lump-sum payments and look for institutional payment plans with low fees. Mindful choices about timing, format, and materials can compound into substantial savings.

- Scholarships and targeted aid

- Used or shared materials

- Payment plans and careful timing

Combine several smaller savings strategies for greater impact. Keep records of what saves money to replicate in future terms.

Financing Options and When to Borrow

Evaluate financing options carefully when savings and payment plans are insufficient. Prioritize interest-free or low-interest institutional plans, employer tuition reimbursement, and targeted educational grants before considering private loans. If borrowing is necessary, compare total cost, repayment terms, and deferment or forbearance rules to avoid long-term payment stress. Use short-term credit sparingly and prefer options that keep monthly obligations predictable.

- Employer tuition reimbursement programs

- Institutional low-interest or interest-free plans

- Avoid high-interest private credit when possible

Choosing the right financing option preserves long-term financial flexibility. Keep paperwork and repayment schedules organized to avoid penalties.

Conclusion

A disciplined, adaptable approach makes education costs manageable alongside other household priorities. Start with a clear assessment, build a recurring budget, and apply targeted cost-reduction tactics. Regular review and small adjustments keep the plan resilient as needs change.