Education expenses can be one of the most persistent line items in a household or individual budget. Understanding the full scope of costs—tuition, fees, supplies and living expenses—is the first step toward a realistic plan. A flexible approach helps absorb unexpected increases and changing priorities over time. This article outlines practical steps to assess costs, control spending, and build durable funding strategies.

Assessing Current Education Costs

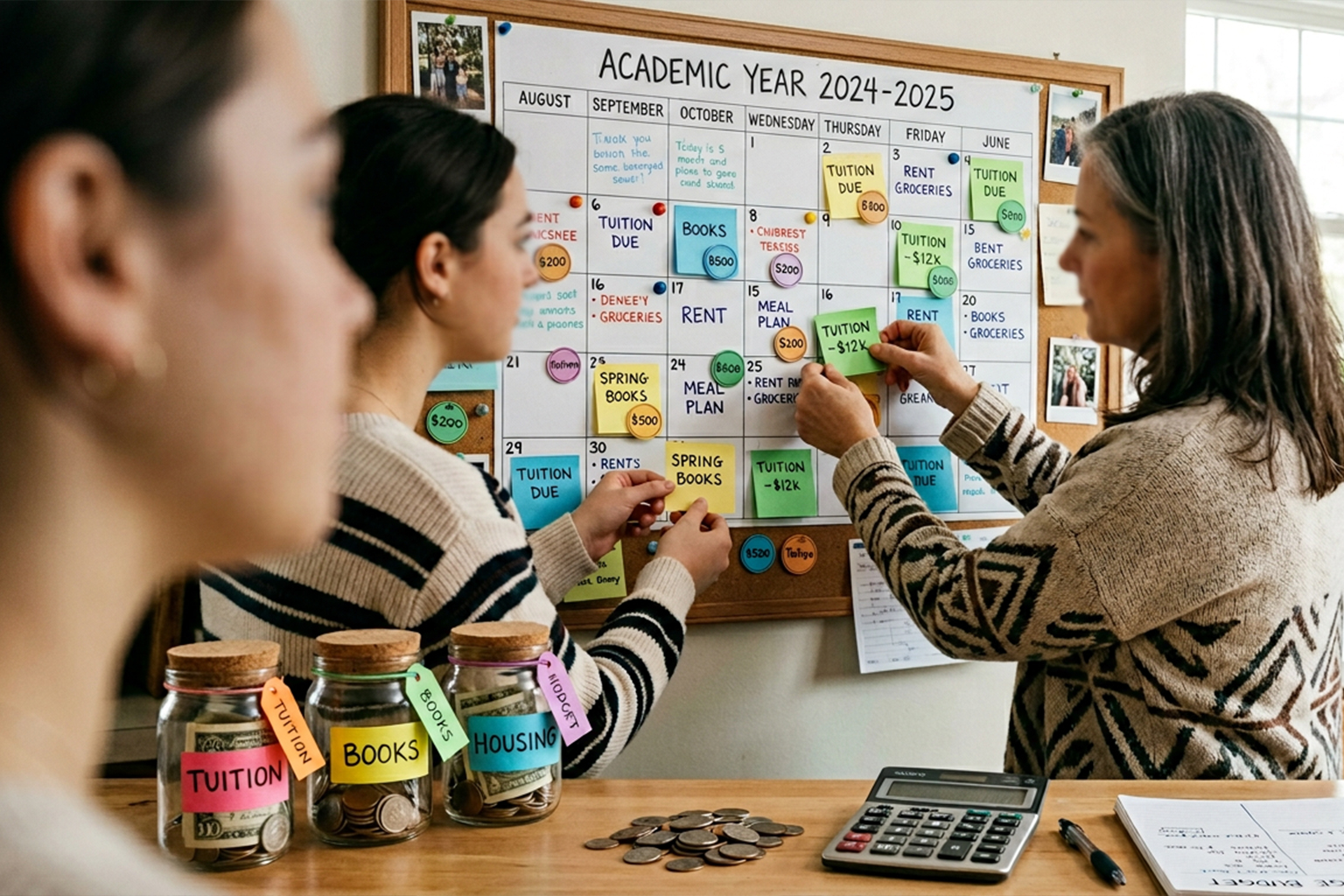

Start by creating a comprehensive snapshot of all education-related spending for the coming year. Include direct costs like tuition and textbooks as well as indirect items such as transportation, technology upgrades, and time invested in coursework. Track historical spending for at least one prior year to identify patterns and seasonal peaks. This baseline makes it easier to set achievable funding targets and prioritize areas for reduction.

Regular review of this snapshot keeps the plan aligned with changing needs. Update estimates whenever program details or living situations change to avoid surprises.

Budgeting and Cost-Control Techniques

Translate your cost assessment into a monthly and annual budget with clear categories. Allocate funds for essentials first and then assign discretionary amounts for extras like enrichment courses or new devices. Use simple tools—spreadsheets or budgeting apps—to automate tracking and alerts. Where feasible, substitute lower-cost alternatives such as used books, shared subscriptions, or online materials to stretch the budget further.

Small, consistent adjustments often prevent large shortfalls later. Encourage contributors or students to participate in budget reviews for greater accountability.

Long-Term Funding and Savings Strategies

Long-term planning involves combining routine savings, targeted funds, and thoughtful borrowing when needed. Establish a dedicated education account to separate short-term savings from emergency reserves and keep growth consistent. Explore employer tuition assistance, scholarships, and community grants that can reduce reliance on loans. When loans are used, compare terms and consider repayment options that match projected income trajectories.

- Automate transfers to a savings account each pay period.

- Prioritize scholarships and work-study opportunities early.

- Reassess loan choices against expected post-study earnings.

Balancing multiple funding sources reduces risk and increases flexibility as circumstances evolve.

Conclusion

Effective management of education expenses begins with a clear, regularly updated picture of costs and a realistic budget. Combining cost-control tactics with steady savings and selective external funding builds resilience. Regular reassessment ensures the plan adapts to life changes and keeps goals within reach.